Arbitrage

Trading strategy exploiting price differences between markets to profit while rebalancing pools to market prices.

Arbitrage in DeFi refers to trading strategies that exploit price discrepancies between different markets or liquidity pools to generate risk-free profit while simultaneously rebalancing prices toward equilibrium. In automated market maker contexts, arbitrageurs play a critical role in maintaining price accuracy by buying underpriced assets from AMM pools and selling overpriced assets into them, aligning pool prices with broader market consensus.

The economic function of arbitrage in traditional markets is well-established—it enforces the law of one price by eliminating profitable opportunities through competition. In DeFi, arbitrage becomes especially important because AMM pools don't directly observe external market prices. Pool prices emerge from internal reserve ratios according to their invariant (e.g., x*y=k). Without arbitrageurs constantly correcting deviations, pool prices would drift arbitrarily from market reality, making the pools unusable for informed trading.

Arbitrage Mechanics in AMMs

Consider an ETH/USDC liquidity pool where ETH trades at 4,000 USDC while the market price on centralized exchanges is 5,000 USDC. An arbitrageur can buy underpriced ETH from the AMM pool at 4,000 USDC and immediately sell it on a CEX for 5,000 USDC, pocketing 1,000 USDC profit per ETH (minus gas and trading fees). This purchase increases the pool's USDC reserves and decreases ETH reserves, shifting the spot price upward toward 5,000 USDC.

The process continues until the profit opportunity disappears. Multiple arbitrageurs compete to capture these opportunities, driving the pool price toward the CEX price through their trading activity. The first arbitrageur might capture most of the profit, while later traders find increasingly marginal opportunities as the prices converge. This competition ensures AMM pools remain reasonably priced despite having no direct price feeds.

Cross-DEX arbitrage exploits price differences between different AMM protocols. If ETH trades at 5,000 USDC on Uniswap but 4,900 USDC on SushiSwap, arbitrageurs buy from SushiSwap and sell to Uniswap, profiting from the 100 USDC difference while equilibrating prices across platforms. Tools like 1inch and DEX aggregators facilitate this by checking prices across many DEXs simultaneously.

Triangular arbitrage finds profit in circular trading paths. If ETH→USDC→DAI→ETH creates a profitable loop (e.g., ending with more ETH than you started), arbitrageurs execute all three swaps atomically. These opportunities arise from temporary pricing inefficiencies across multiple pairs and are typically captured within seconds of appearing.

Flash Loans and Capital-Free Arbitrage

Flash loans revolutionized DeFi arbitrage by eliminating capital requirements. Traditionally, arbitrageurs needed substantial capital to execute profitable trades—exploiting a 1% price difference might require $1 million to generate $10,000 profit. Flash loans enable borrowing unlimited capital (up to pool capacity) with zero collateral, provided repayment occurs within the same transaction.

An arbitrage transaction using flash loans follows this pattern: borrow 1,000 ETH from Aave via flash loan, sell 1,000 ETH on DEX A for USDC at a higher price, buy 1,005 ETH on DEX B with the USDC at a lower price, repay the 1,000 ETH flash loan plus a small fee, and keep the 5 ETH profit. If any step fails or the arbitrage isn't profitable, the entire transaction reverts atomically, preventing losses.

This capital efficiency dramatically increased arbitrage competition. Anyone with technical skills can execute arbitrage regardless of wealth, democratizing market making while also enabling more sophisticated MEV extraction. The downside is that flash loan-enabled arbitrage can be more aggressive, extracting value that might otherwise accumulate to traders or liquidity providers.

Arbitrage as Attack Vector

While arbitrage provides essential price discovery, it also imposes costs. Impermanent loss for liquidity providers is fundamentally caused by arbitrageurs. When market prices move, arbitrageurs trade against the pool to rebalance it, buying the asset that decreased in price and selling the asset that increased. This forces LPs to sell winners and buy losers, crystallizing losses relative to simply holding the assets.

From the LP perspective, arbitrageurs are extracting value—the profit arbitrageurs earn comes from the LPs' pockets. Yet this extraction is necessary for the pool to remain useful. Without arbitrage, pool prices would be wildly incorrect, deterring legitimate traders. The trading fees LPs earn are compensation for providing liquidity that enables both legitimate trading and arbitrage extraction.

Just-In-Time (JIT) liquidity is an advanced arbitrage strategy where sophisticated actors add liquidity immediately before large trades, capture fees from those trades, then remove liquidity—minimizing exposure to impermanent loss while still earning fees. This technique is particularly relevant in Uniswap V3 where concentrated liquidity enables extremely capital-efficient JIT positions.

Sandwich attacks weaponize arbitrage for MEV extraction. An attacker observes a pending trade in the mempool, front-runs it with a trade that moves the price against the victim, lets the victim's transaction execute at a worse price, then back-runs with a reverse trade to profit from the price movement. This is technically arbitrage (profiting from a price discrepancy the attacker created), but it's adversarial rather than beneficial.

Detecting and Extracting Arbitrage Opportunities

Arbitrage bots continuously monitor blockchain state and mempools for profitable opportunities. These bots calculate expected profit considering gas costs, slippage, and competition. During periods of high gas prices, only large arbitrage opportunities are economically viable, potentially leaving smaller discrepancies unaddressed and causing temporary price inaccuracies.

MEV (Maximal Extractable Value) auction platforms like Flashbots have formalized arbitrage extraction. Searchers compete by bidding in auctions to include their arbitrage transactions in specific block positions, with proceeds split between the searcher and the block builder. This creates a competitive marketplace for arbitrage execution while reducing on-chain spam from failed attempts.

Private transaction pools enable searchers to submit arbitrage transactions without revealing them in the public mempool, preventing frontrunning of their own trades. Flashbots protect searchers allow submitting bundles that either succeed atomically or don't appear on-chain at all, eliminating gas waste from failed arbitrage attempts.

Statistical Arbitrage and Directional Betting

Statistical arbitrage exploits correlations between assets rather than direct price discrepancies. If ETH and BTC historically maintain a certain price ratio and that ratio temporarily diverges, a stat arb strategy might bet on mean reversion by trading one asset against the other. This is riskier than pure arbitrage since correlations can break down, but it can be profitable in mean-reverting markets.

Latency arbitrage leverages speed advantages to capture opportunities before competitors. In traditional finance, this involves physical proximity to exchanges (co-location). In DeFi, it's about monitoring mempool, having efficient code, and potentially paying higher gas prices to ensure fast execution. The arms race for latency has led to increasingly sophisticated bot infrastructure.

Understanding arbitrage is crucial for DeFi security and protocol design. The article emphasizes that arbitrage causes impermanent loss—the fundamental economic risk for liquidity providers. Protocols must design incentive structures acknowledging that arbitrageurs will extract value from price movements. Fee structures should compensate LPs adequately for this extraction, and security analysis should consider whether arbitrage mechanisms can be exploited to attack the protocol (oracle manipulation, sandwich attacks, etc.). Arbitrage is simultaneously essential for price accuracy and a vector for value extraction, requiring careful consideration in both protocol economics and security modeling.

Articles Using This Term

Learn more about Arbitrage in these articles:

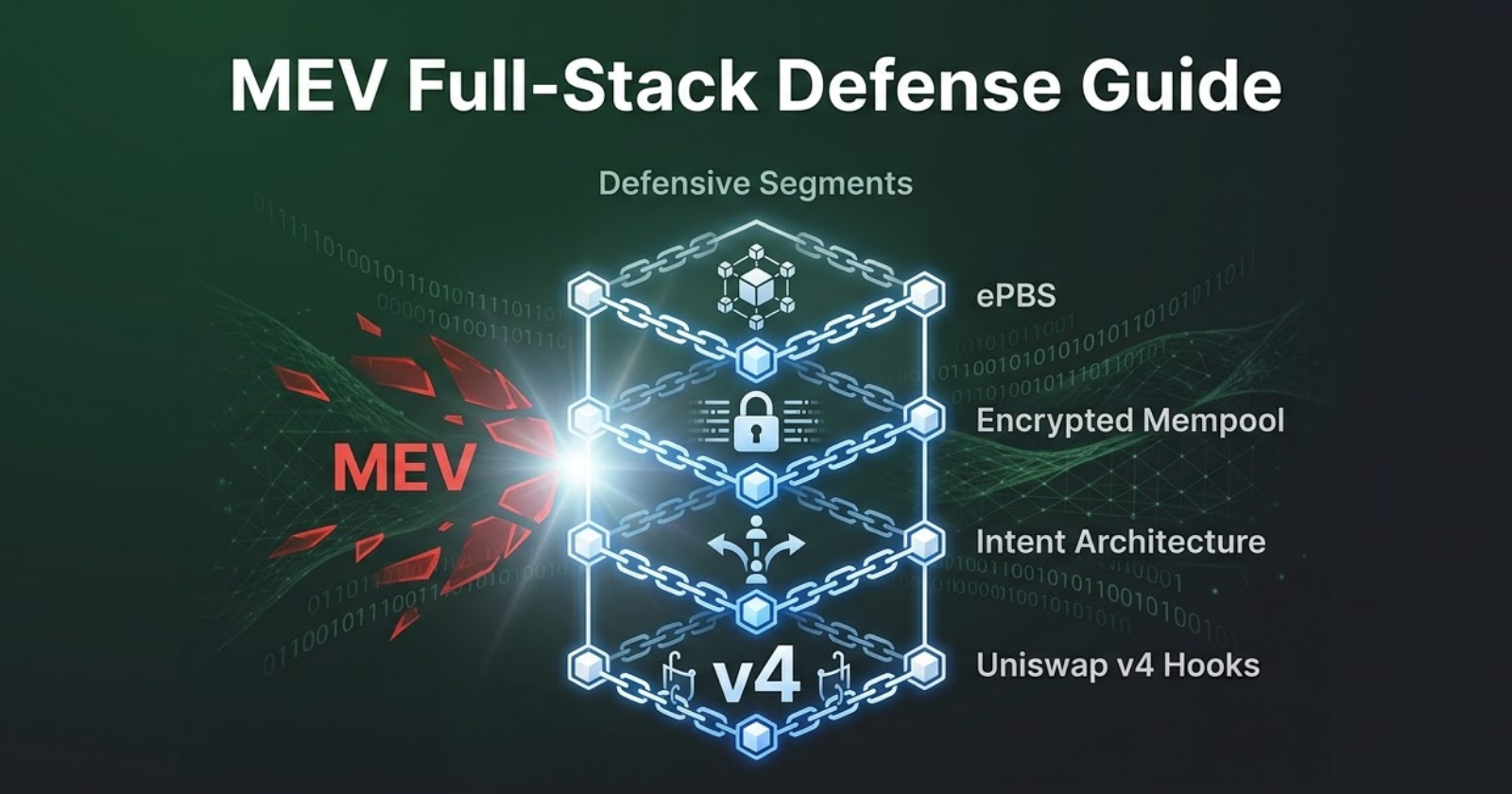

How to protect your DeFi protocol from MEV: A full-stack defense guide

Learn how to defend your DeFi protocol from sandwich attacks and MEV extraction with PBS, encrypted mempools, intent architectures, and Uniswap v4 hooks.

AMM Security Foundations: Master DeFi Trading Risks

Deep dive into the foundations of constant-product AMMs. Learn the math, smart contract building blocks, and core security risks behind decentralized trading protocols.

Related Terms

Liquidity Pool

Smart contract holding reserves of two or more tokens that enable decentralized trading without order books.

Impermanent Loss

The temporary loss in value experienced by liquidity providers when the price ratio of deposited assets changes compared to holding them.

MEV (Maximal Extractable Value)

Profit extracted by reordering, including, or excluding transactions within a block.

Flash Loan

Uncollateralized loan borrowed and repaid within a single transaction, often used for arbitrage or attacks.

Need expert guidance on Arbitrage?

Our team at Zealynx has deep expertise in blockchain security and DeFi protocols. Whether you need an audit or consultation, we're here to help.

Get a Quote